By: Edward Ambrose

Summary

Microsoft grew revenue by 14% and operating income by 21%. This strong growth is continuing.

The Cloud and commercial applications are the higher growth and margin parts of the business.

The growth is driven by high research and development and guaranteed by $134 billion of cash, which can be used for acquisitions. It is a strong buy.

The knock on Microsoft (MSFT) is that the new CEO, Satya Nadella, cleaned house and brought the company back, but the stock is no longer cheap, and its old franchises, Windows and Office, are low-growth businesses. All this is true, but it is beside the point. Windows and Office grew at 7-8 percent in the fiscal year ending June 30. However, Microsoft grew at 14% due to cloud and cloud-related products. The stock is more expensive, and its P/E is 28. However, the growth makes it a strong buy.

Microsoft Results

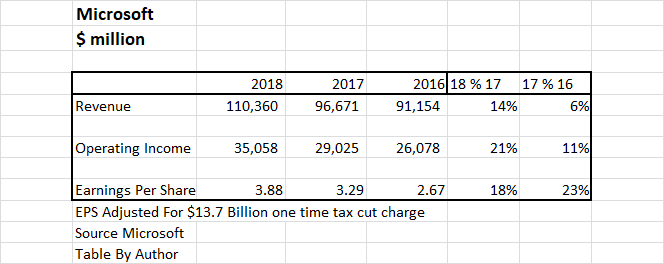

Microsoft’s income is summarized below for the last three years. Revenue in 2018 grew 14%, exceeding $100 billion for the first time, with operating income up 21%. The tax cut caused a one-time tax charge of $13.7 billion. Without adjusting for this charge, the P/E would be 50 rather than 28.

The rapid growth in volume has led to even higher growth in operating income. Another 18% increase in earnings per share would make Microsoft a trillion-dollar market cap company.

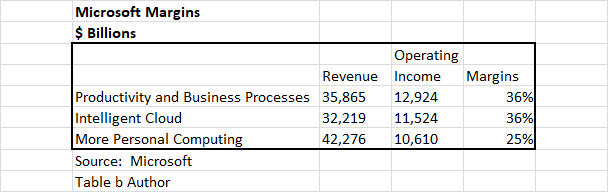

Microsoft Brands

The business is divided into the three groups shown in the table below. Both the Productivity Business Processes and the Intelligent Cloud have margins of 36%. The More Personal Computing margins are lower at a still respectable 25%.